| Name |

Characteristics |

| Panic of 1785 |

1785–1788 |

The panic of 1785, which lasted until 1788, ended the business boom that

followed the American Revolution. The causes of the crisis lay in the

overexpansion and debts incurred after the victory at Yorktown, a postwar

deflation, competition in the manufacturing sector from Britain, and lack of

adequate credit and a sound currency. The downturn was exacerbated by the

absence of any significant interstate trade. Other factors were the British

refusal to conclude a commercial treaty, and actual and pending defaults

among debtor groups. The panic among business and propertied groups led to

the demand for a stronger federal government. |

|

Copper Panic of 1789 |

17961789–1793 |

Loss of confidence in copper coins due to debasement and counterfeiting

led to commercial freeze up that halted the economy of several northern

States and was not alleviated until the introduction of new paper money to

restore confidence. |

|

Panic of 1797 |

17961796–1799 |

Just as a land speculation bubble was bursting, deflation from the

Bank of England (which was facing insolvency because of the cost of

Great Britain's involvement in the

French Revolutionary Wars) crossed to North America and disrupted

commercial and

real

estate markets in the United States and the

Caribbean,

and caused a

major financial panic.[10]

Prosperity continued in the south, but economic activity was stagnant in the

north for three years. The young United States engaged in the

Quasi-War

with France.[8] |

| 1802–1804 recession |

18021802–1804 |

A boom of war-time activity led to a decline after the

Peace of Amiens ended the

war between the United Kingdom and France. Commodity prices fell

dramatically. Trade was disrupted by pirates, leading to the

First Barbary War.[8] |

| Depression of 1807 |

18071807–1810 |

The

Embargo Act of 1807 was passed by the

United States Congress under President

Thomas Jefferson as tensions increased with the United Kingdom. Along

with trade restrictions imposed by the British, shipping-related industries

were hard hit. The

Federalists fought the embargo and allowed smuggling to take place in

New

England. Trade volumes, commodity prices and securities prices all began

to fall.

Macon's Bill Number 2 ended the embargoes in May 1810, and a recovery

started.[8] |

| 1812 recession |

18121812 |

The United States entered a brief recession at the beginning of 1812.

The decline was brief primarily because the United States soon increased

production to fight the

War

of 1812, which began June 18, 1812.[11] |

| 1815–21 depression |

18151815–1821 |

Shortly after the war ended on March 23, 1815, the United States entered

a period of financial panic as bank notes rapidly depreciated because of

inflation following the war. The 1815 panic was followed by several years of

mild depression, and then a major financial crisis – the

Panic of 1819, which featured widespread

foreclosures, bank failures,

unemployment, a collapse in real estate prices, and a slump in

agriculture and

manufacturing.[8] |

| 1822–1823 recession |

18221822–1823 |

After only a mild recovery following the lengthy 1815–21 depression,

commodity prices hit a peak in March 1822 and began to fall. Many businesses

failed, unemployment rose and an increase in imports worsened the trade

balance.[8] |

| 1825–1826 recession |

18251825–1826 |

The

Panic of 1825, a stock crash following a bubble of speculative

investments in Latin America led to a decline in business activity in the

United States and England. The recession coincided with a major panic, the

date of which may be more easily determined than general cycle changes

associated with other recessions.[7] |

| 1828–1829 recession |

18281828–1829 |

In 1826, England forbade the United States to trade with English

colonies, and in 1827, the United States adopted a counter-prohibition.

Trade declined, just as credit became tight for manufacturers in New

England.[8] |

| 1833–34 recession |

18331833–1834 |

The United States' economy declined moderately in 1833–34. News accounts

of the time confirm the slowdown. The subsequent expansion was driven by

land speculation.[12] |

US recessions, Free Banking Era to the Great Depression

| Name |

Characteristics |

| 1836–1838 recession |

-32.8% |

— |

A sharp downturn in the

American economy was caused by bank failures and lack of confidence in

the paper

currency. Speculation markets were greatly affected when

American banks stopped payment in

specie

(gold and silver coinage).[3][13]

Over 600 banks failed in this period. In the South, the cotton market

completely collapsed.[8]

See:

Panic of 1837 |

| late 1839–late 1843 recession |

-34.3% |

— |

This was one of the longest and deepest depressions. It was a period of

pronounced

deflation

and massive default on debt. The Cleveland Trust Company Index showed the

economy spent 68 months below its trend and only 9 months above it. The

Index declined 34.3% during this depression.[14] |

| 1845–late 1846 recession |

−5.9% |

— |

This recession was mild enough that it may have only been a slowdown in

the growth cycle. One theory holds that this would have been a recession,

except the United States began to gear up for the

Mexican–American War, which began April 25, 1846.[15] |

| 1847–48 recession |

−19.7% |

— |

The Cleveland Trust Company Index declined 19.7% during 1847 and 1848.

It is associated with a

financial crisis in Great Britain.[14][16] |

|

1853–54 recession |

−18.4% |

— |

Interest rates rose in this period, contributing to a decrease in

railroad investment. Security prices fell during this period. With the

exception of falling business investment there is little evidence of

contraction in this period.[3] |

|

Panic of 1857 |

−23.1% |

— |

Failure of the

Ohio Life Insurance and Trust Company burst a European speculative

bubble in

United States' railroads and caused a loss of confidence in

American banks. Over 5,000 businesses failed within the first year of

the Panic, and unemployment was accompanied by protest meetings in urban

areas. This is the earliest recession to which the NBER assigns specific

months (rather than years) for the peak and trough.[5][7][17] |

| 1860–61 recession |

−14.5% |

— |

There was a recession before the

American Civil War, which began April 12, 1861. Zarnowitz says the data

generally show a contraction occurred in this period, but it was quite mild.[14]

A financial panic was narrowly averted in 1860 by the first use of

clearing house certificates between banks.[8] |

| 1865–67 recession |

−23.8% |

— |

The

American Civil War ended in April 1865, and the country entered a

lengthy period of general deflation that lasted until 1896. The United

States occasionally experienced periods of recession during the

Reconstruction era. Production increased in the years following the

Civil War, but the country still had financial difficulties.[14]

The post-war period coincided with a period of some

international financial instability. |

| 1869–70 recession |

−9.7% |

— |

A few years after the Civil War, a short recession occurred. It was

unusual since it came amid a period when railroad investment was greatly

accelerating, even producing the

First Transcontinental Railroad. The railroads built in this period

opened up the interior of the country, giving birth to the

Farmers' movement. The recession may be explained partly by ongoing

financial difficulties following the war, which discouraged businesses from

building up inventories.[14]

Several months into the recession, there was a

major financial panic. |

|

Panic of 1873 and the

Long Depression |

−33.6% (−27.3%)

[nb 3] |

— |

Economic problems in Europe prompted the failure of

Jay Cooke

& Company, the largest bank in the United States, which burst the post-Civil

War

speculative bubble. The

Coinage Act of 1873 also contributed by immediately depressing the price

of silver, which hurt North American mining interests.[18]

The deflation and wage cuts of the era led to labor turmoil, such as the

Great Railroad Strike of 1877. In 1879, the United States returned to

the gold standard with the

Specie Payment Resumption Act. This is the longest period of economic

contraction recognized by the NBER. The

Long Depression is sometimes held to be the entire period from 1873–96.[19][20] |

|

1882–85 recession |

−32.8% |

−24.6% |

Like the Long Depression that preceded it, the recession of 1882–85 was

more of a

price depression than a production depression. From 1879 to 1882, there

had been a boom in railroad construction which came to an end, resulting in

a decline in both railroad construction and in related industries,

particularly iron and steel.[21]

A major economic event during the recession was the

Panic of 1884. |

| 1887–88 recession |

−14.6% |

−8.2% |

Investments in railroads and buildings weakened during this period. This

slowdown was so mild that it is not always considered a recession.

Contemporary accounts apparently indicate it was considered a slight

recession.[22] |

| 1890–91 recession |

−22.1% |

−11.7% |

Although shorter than the recession in 1887–88 and still modest, a

slowdown in 1890–91 was somewhat more pronounced than the preceding

recession. International monetary disturbances are blamed for this

recession, such as the

Panic of 1890 in the United Kingdom.[22] |

|

Panic of 1893 |

−37.3% |

−29.7% |

Failure of the United States

Reading Railroad and withdrawal of European investment led to a

stock market and banking collapse. This Panic was also precipitated in

part by a

run on the gold supply. The Treasury had to issue bonds to purchase

enough gold. Profits, investment and income all fell, leading to political

instability, the height of

the U.S. populist movement and the

Free Silver movement.[23] |

|

Panic of 1896 |

−25.2% |

−20.8% |

The period of 1893–97 is seen as a generally depressed cycle that had a

short spurt of growth in the middle, following the Panic of 1893. Production

shrank and deflation reigned.[22] |

| 1899–1900 recession |

−15.5% |

−8.8% |

This was a mild recession in the period of general growth beginning

after 1897. Evidence for a recession in this period does not show up in some

annual data series.[22] |

| 1902–04 recession |

−16.2% |

−17.1% |

Though not severe, this downturn lasted for nearly two years and saw a

distinct decline in the national product. Industrial and commercial

production both declined, albeit fairly modestly.[22]

The recession came about a year after a

1901 stock crash. |

|

Panic of 1907 |

−29.2% |

−31.0% |

A run on

Knickerbocker Trust Company deposits on October 22, 1907, set events in

motion that would lead to a severe monetary contraction. The fallout from

the panic led to Congress

creating the Federal Reserve System.[24] |

|

Panic of 1910–1911 |

−14.7% |

−10.6% |

This was a mild but lengthy recession. The national product grew by less

than 1%, and commercial activity and industrial activity declined. The

period was also marked by deflation.[22] |

| Recession of 1913–1914 |

−25.9% |

−19.8% |

Productions and real income declined during this period and were not

offset until the start of

World

War I increased demand.[22]

Incidentally, the

Federal Reserve Act was signed during this recession, creating the

Federal Reserve System, the culmination of a sequence of events

following the

Panic of 1907.[24] |

|

Post-World War I recession |

−24.5% |

−14.1% |

Severe

hyperinflation in Europe took place over production in North America.

This was a brief but very sharp recession and was caused by the end of

wartime production, along with an influx of labor from returning troops.

This, in turn, caused high unemployment.[25] |

|

Depression of 1920–21 |

−38.1% |

−32.7% |

The 1921 recession began a mere 10 months after the post-World War I

recession, as the economy continued working through the shift to a peacetime

economy. The recession was short, but extremely painful. The year 1920 was

the single most deflationary year in American history; production, however,

did not fall as much as might be expected from the deflation. GNP may have

declined between 2.5 and 7 percent, even as wholesale prices declined by

36.8%.[26]

The economy had a strong recovery following the recession.[27] |

| 1923–24 recession |

−25.4% |

−22.7% |

From the depression of 1920–21 until the Great Depression, an era dubbed

the

Roaring Twenties, the economy was generally expanding. Industrial

production declined in 1923–24, but on the whole this was a mild recession.[22] |

| 1926–27 recession |

−12.2% |

−10.0% |

This was an unusual and mild recession, thought to be caused largely

because

Henry Ford closed production in his factories for six months to switch

from production of the

Model T to the

Model A.

Charles P. Kindleberger says the period from 1925 to the start of the

Great Depression is best thought of as a boom, and this minor recession just

proof that the boom "was not general, uninterrupted or extensive".[28] |

| |

Characteristics |

|

Great Depression |

1929Aug

1929 –

Mar 1933 |

24.924.9%[32]

(1933) |

26.7−26.7% |

Stock markets crashed worldwide. A banking collapse took place in the

United States.

Extensive new tariffs and

other factors contributed to an extremely deep depression. The United

States did remain in a depression until World War II. In 1936, unemployment

fell to 16.9%, but later returned to 19% in 1938 (near 1933 levels). |

|

Recession of 1937–1938 |

1937May

1937 –

June 1938 |

19.019.0%[33]

(1938) |

03.4−18.2% |

The

Recession of 1937 is only considered minor when compared to the Great

Depression, but is otherwise among the worst recessions of the 20th century.

Three explanations are offered for the recession: that tight fiscal policy

from an attempt to balance the budget after the expansion of the

New Deal

caused recession, that tight monetary policy from the Federal Reserve caused

the recession, or that declining profits for businesses led to a reduction

in investment.[34] |

| Recession of 1945 |

1945Feb–Oct

1945 |

05.25.2%[33]

(1946) |

12.7−12.7% |

The decline in government spending at the end of World War II led to an

enormous drop in gross domestic product, making this technically a

recession. This was the result of demobilization and the shift from a

wartime to peacetime economy. The post-war years were unusual in a number of

ways (unemployment was never high) and this era may be considered a "sui

generis end-of-the-war recession".[35] |

|

Recession of 1949 |

1948Nov

1948 –

Oct 1949 |

07.97.9%

(Oct 1949) |

01.7−1.7% |

The 1948 recession was a brief economic downturn; forecasters of the

time expected much worse, perhaps influenced by the poor economy in their

recent lifetimes.[36]

The recession also followed a period of monetary tightening.[30] |

|

Recession of 1953 |

1953July

1953 –

May 1954 |

06.16.1%

(Sep 1954) |

02.6−2.6% |

After a post-Korean

War inflationary period, more funds were transferred to

national security. In 1951, the Federal Reserve

reasserted its independence from the U.S. Treasury and in 1952, the

Federal Reserve changed monetary policy to be more restrictive because of

fears of further inflation or of a

bubble forming.[30][37][38] |

|

Recession of 1958 |

1957Aug

1957 –

April 1958 |

.57.5%

(July 1958) |

03.1−3.7% |

Monetary policy was tightened during the two years preceding 1957,

followed by an easing of policy at the end of 1957. The budget balance

resulted in a change in

budget surplus of 0.8% of GDP in 1957 to a

budget deficit of 0.6% of GDP in 1958, and then to 2.6% of GDP in 1959.[30] |

|

Recession of 1960–61 |

1960Apr

1960 –

Feb 1961 |

17.1%

(May 1961) |

01.6−1.6% |

Another primarily monetary recession occurred after the Federal Reserve

began raising interest rates in 1959. The government switched from deficit

(or 2.6% in 1959) to surplus (of 0.1% in 1960). When the economy emerged

from this short recession, it began the second-longest period of growth in

NBER history.[30]

The Dow Jones Industrial Average (Dow) finally reached its lowest point on

Feb. 20, 1961, about 4 weeks after President Kennedy was inaugurated. |

|

Recession of 1969–70 |

1969Dec

1969 –

Nov 1970 |

6.1%

(Dec 1970) |

00.6−0.6% |

The relatively mild 1969 recession followed a lengthy expansion. At the

end of the expansion, inflation was rising, possibly a result of increased

deficits. This relatively mild recession coincided with an attempt to start

closing the budget deficits of the

Vietnam War (fiscal tightening) and the Federal Reserve raising interest

rates (monetary tightening).[30] |

|

1973–75 recession |

1973Nov

1973 –

Mar 1975 |

9.0%

(May 1975) |

03.2−3.2% |

A quadrupling of oil prices by

OPEC coupled

with high government spending because of the Vietnam War led to

stagflation in the United States.[39]

The period was also marked by the

1973 oil crisis and the

1973–1974 stock market crash. The period is remarkable for rising

unemployment coinciding with rising inflation.[40] |

|

1980 recession |

1980Jan–July

1980 |

7.8%

(July 1980) |

02.2−2.2% |

The NBER considers a very short recession to have occurred in 1980,

followed by a short period of growth and then a deep recession. Unemployment

remained relatively elevated in between recessions. The recession began as

the Federal Reserve, under

Paul Volcker, raised interest rates dramatically to fight the

inflation of the 1970s. The early '80s are sometimes referred to as a "double-dip"

or "W-shaped"

recession.[30][41] |

|

Early 1980s recession |

1981July

1981 –

Nov 1982 |

10.8%

(Nov 1982) |

02.7−2.7% |

The

Iranian Revolution sharply increased the price of oil around the world

in 1979, causing the

1979 energy crisis. This was caused by the new regime in power in

Iran, which

exported oil at inconsistent intervals and at a lower volume, forcing prices

up. Tight

monetary policy in the United States to control inflation led to another

recession. The changes were made largely because of inflation carried over

from the previous decade because of the

1973 oil crisis and the 1979 energy crisis.[42][43] |

|

Early 1990s recession |

1990July

1990 –

Mar 1991 |

7.8%

(June 1992) |

01.4−1.4% |

After the lengthy peacetime expansion of the 1980s, inflation began to

increase and the Federal Reserve responded by raising interest rates from

1986 to 1989. This weakened but did not stop growth, but some combination of

the subsequent

1990 oil price shock, the debt accumulation of the 1980s, and growing

consumer pessimism combined with the weakened economy to produce a brief

recession.[44][45][46] |

|

Early 2000s recession |

2001March

2001–Nov 2001 |

6.3%

(June 2003) |

00.3−0.3% |

The 1990s were the longest period of growth in American history. The

collapse of the speculative

dot-com bubble, a fall in business outlays and investments, and the

September 11th attacks,[47]

brought the decade of growth to an end. Despite these major shocks, the

recession was brief and shallow.[48]

Without the September 11th attacks, the economy might have avoided recession

altogether.[47

] |

|

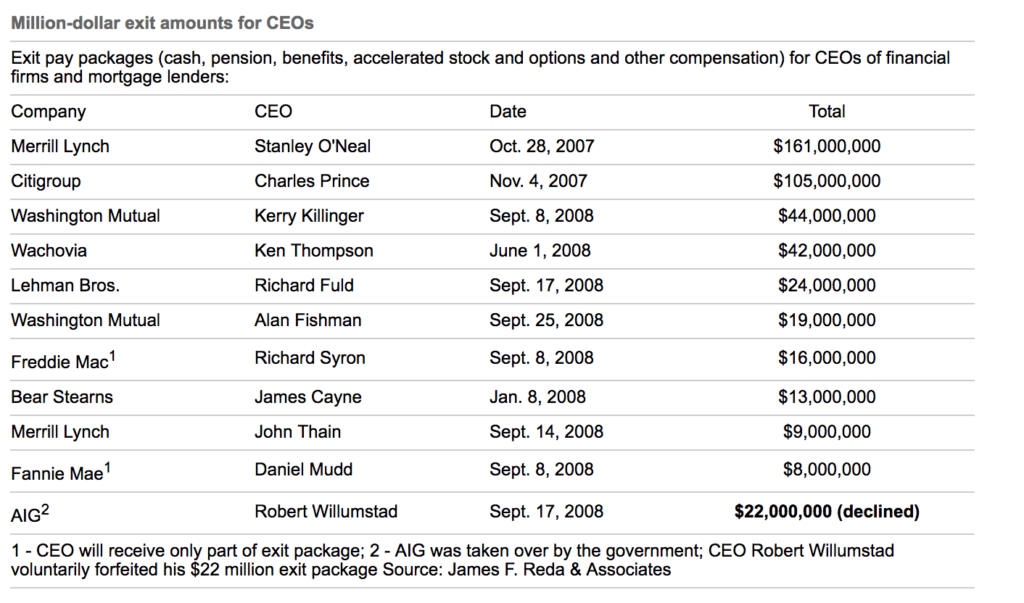

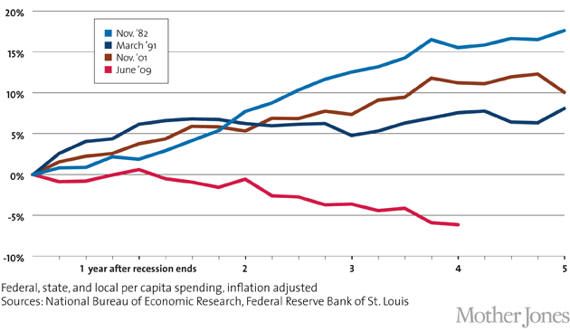

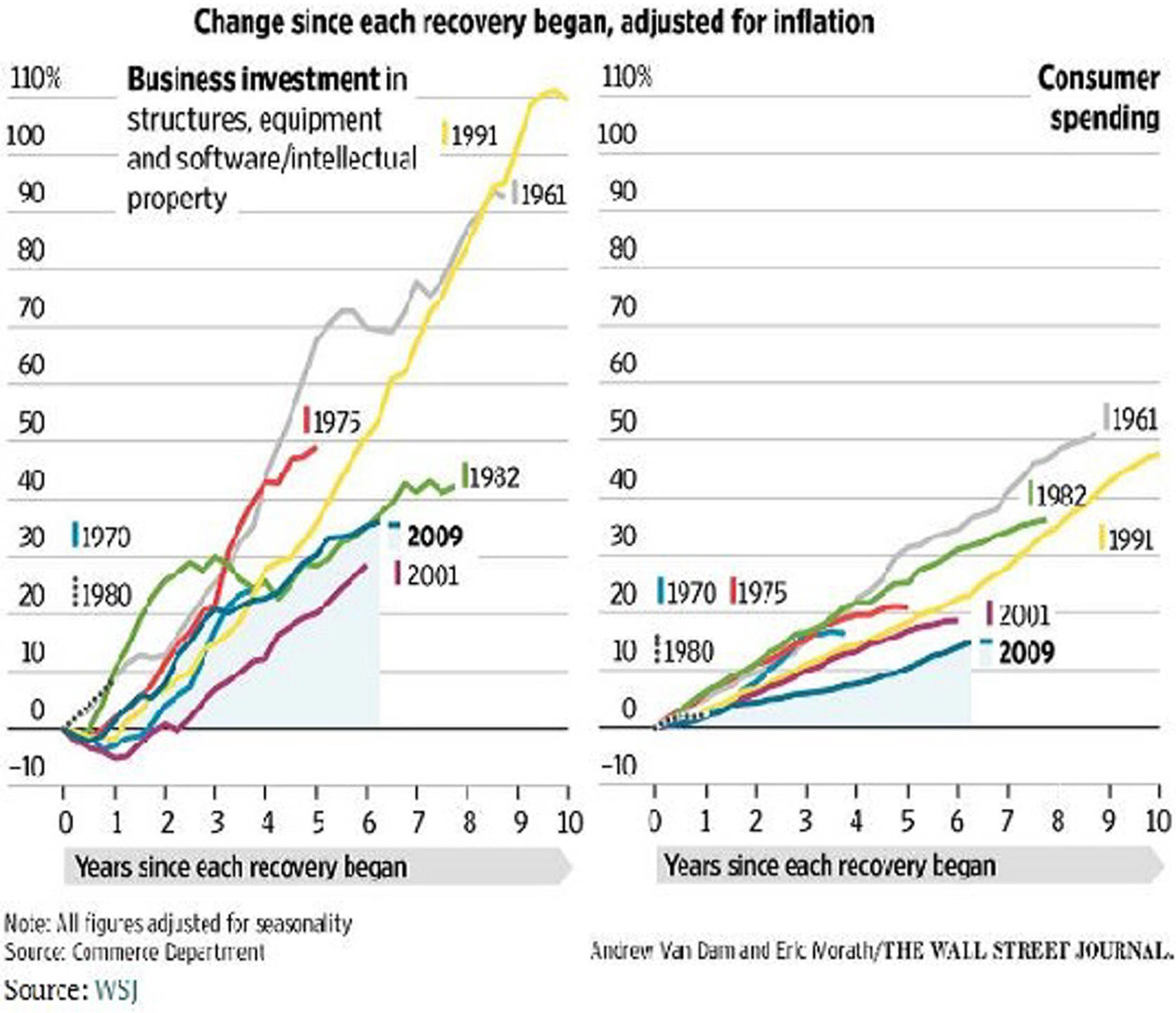

Great Recession |

2007Dec

2007 – June 2009[49][50] |

10.0%

(October 2009)[51] |

03.9−4.3% |

The

subprime mortgage crisis led to the collapse of the

United States housing bubble. Falling housing-related assets contributed

to a

global financial crisis, even as oil and food prices soared. The crisis

led to the failure or collapse of many of the United States' largest

financial institutions:

Bear Stearns,

Fannie

Mae,

Freddie Mac,

Lehman Brothers, City Bank and

AIG, as well as a crisis in the

automobile industry. The government responded with an unprecedented

$700 billion bank bailout and

$787 billion fiscal stimulus package. The National Bureau of Economic

Research declared the end of this recession over a year after the end date.[52]

The Dow Jones Industrial Average (Dow)

finally reached its lowest point on March 9, 2009.[ |

{kind=link}

.svg){kind=link}